Democratizing Private Equity Opportunities with Evergreen Funds

Intelligent investors aim for two objectives: 1) achieving the appropriate level of return to meet their financial goals, and 2) managing the necessary level of risk to attain those returns.

As discussed elsewhere, the return outlook in public markets is diminishing, while political and economic risks continue to rise. This has prompted many investors to look towards private markets, particularly private equity (PE), as a means to sustain returns while mitigating risk through diversification.

The Challenges of PE

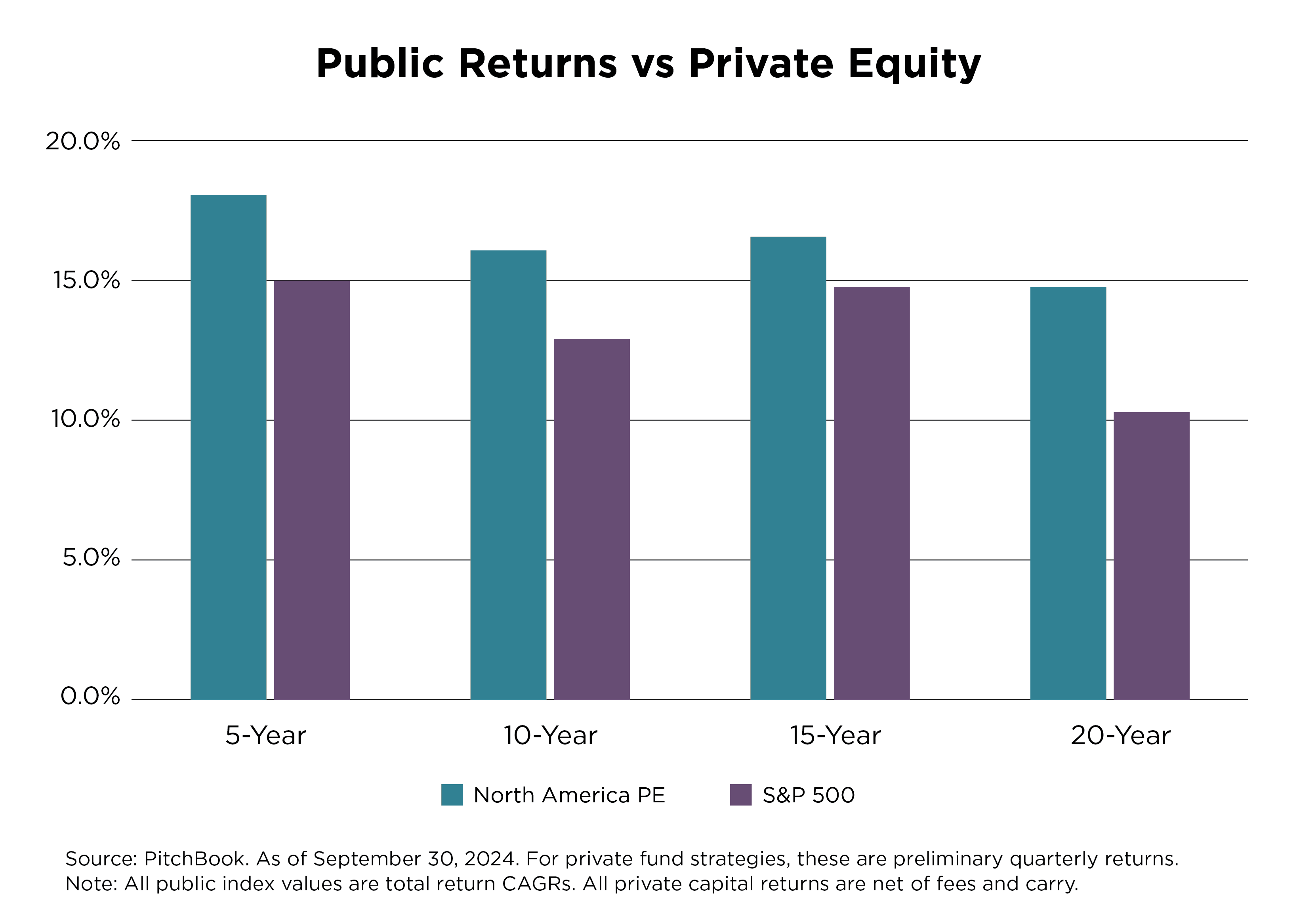

PE is often touted for its exceptional returns compared to other asset classes.[1]

However, the real challenge lies in implementation. In simple terms, accessing PE funds is not easy for individual investors.

The primary issue is that most PE funds target institutional investors with larger sums of capital. This often results in a high minimum investment requirement, typically a seven-figure amount (e.g., $5 million).

Moreover, to reduce risk, most PE investors often diversify their capital across 10 to 20 funds. Even assuming a modest investment of $2.5 million per fund, this amounts to a total commitment of $25 million to $50 million.

Furthermore, PE funds generally lock up investor capital for the duration of the fund’s life, which typically lasts 10-12 years. This makes PE largely inaccessible for non-institutional investors who are unable to make such significant capital commitments.

The Role of Evergreen Funds

This limited access is a genuine issue. Given that 99% of companies are privately held, the private markets present a far greater number of investment opportunities compared to the public markets. The missing link until recently was a mechanism to gather and deploy the capital of thousands of individual investors and take advantage of these opportunities.

Enter evergreen funds. Unlike traditional “drawdown” funds, which have a fixed lifecycle (raise capital, deploy capital, return capital), evergreen funds are perpetual, allowing investors to add and withdraw funds with much more flexibility, without the decade-long lock-up periods typical of traditional funds.

Perhaps most importantly, evergreen funds often feature much lower minimum investment thresholds, sometimes as low as $25,000, making them accessible to affluent investors who may not have the capital required for traditional PE funds.

Additionally, evergreen funds acting as “multi-managers” offer access to top-tier traditional PE funds, which might otherwise be inaccessible to individual investors. This is crucial, as there is a substantial difference in performance between various PE funds. Securing access to a top-quartile PE fund could generate returns as much as 14% higher annually compared to a bottom-quartile fund.[2]

Evaluating the Trade-Offs

At this point, it's natural to question whether the benefits of evergreen funds come at a cost. Is the higher liquidity they offer too good to be true? And are the high minimum investments in traditional funds really there for a reason?

Both observations hold some merit.

It is true that offering higher liquidity comes with a cost. In evergreen funds, part of the invested capital is held in a “liquidity sleeve” to ensure there are funds available for investors who wish to withdraw. This liquid portion of the fund typically earns lower returns, which impacts overall fund performance.

Additionally, evergreen funds are subject to more regulations and have unique operational complexities, particularly ensuring that capital inflows and outflows do not disrupt the fund’s operations, leading to higher costs for the investor.

However, these challenges are mitigated by two significant advantages:

Diversification: The flexibility of the evergreen model allows for diversification across sectors, managers, and geographies, thus lowering the overall risk of the investment.

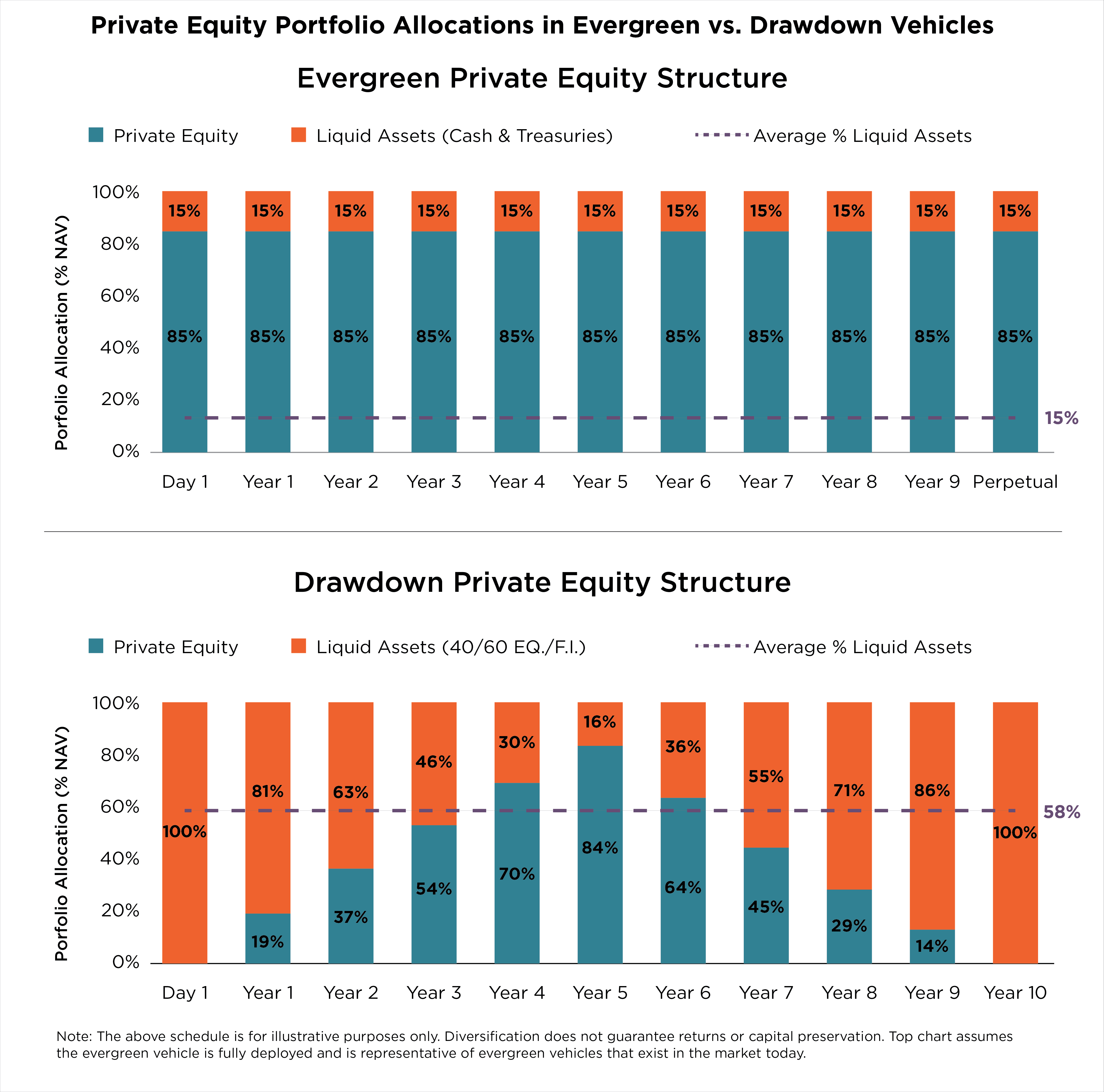

Efficient Capital Deployment: Unlike traditional “drawdown” PE models, where capital often remains idle for extended periods, evergreen funds put investor capital to work from day one. The contrast is shown in the chart below, with the blue portion denoting “actively deployed capital” - in other words, genuine “private equity”.

Source: Kohlberg Kravis Roberts & Co.

The traditional drawdown structure in private equity typically leads to a slow start, resulting in the “J-curve” phenomenon, where returns may be low or even negative in the early years of a fund. The evergreen model, however, avoids this issue.

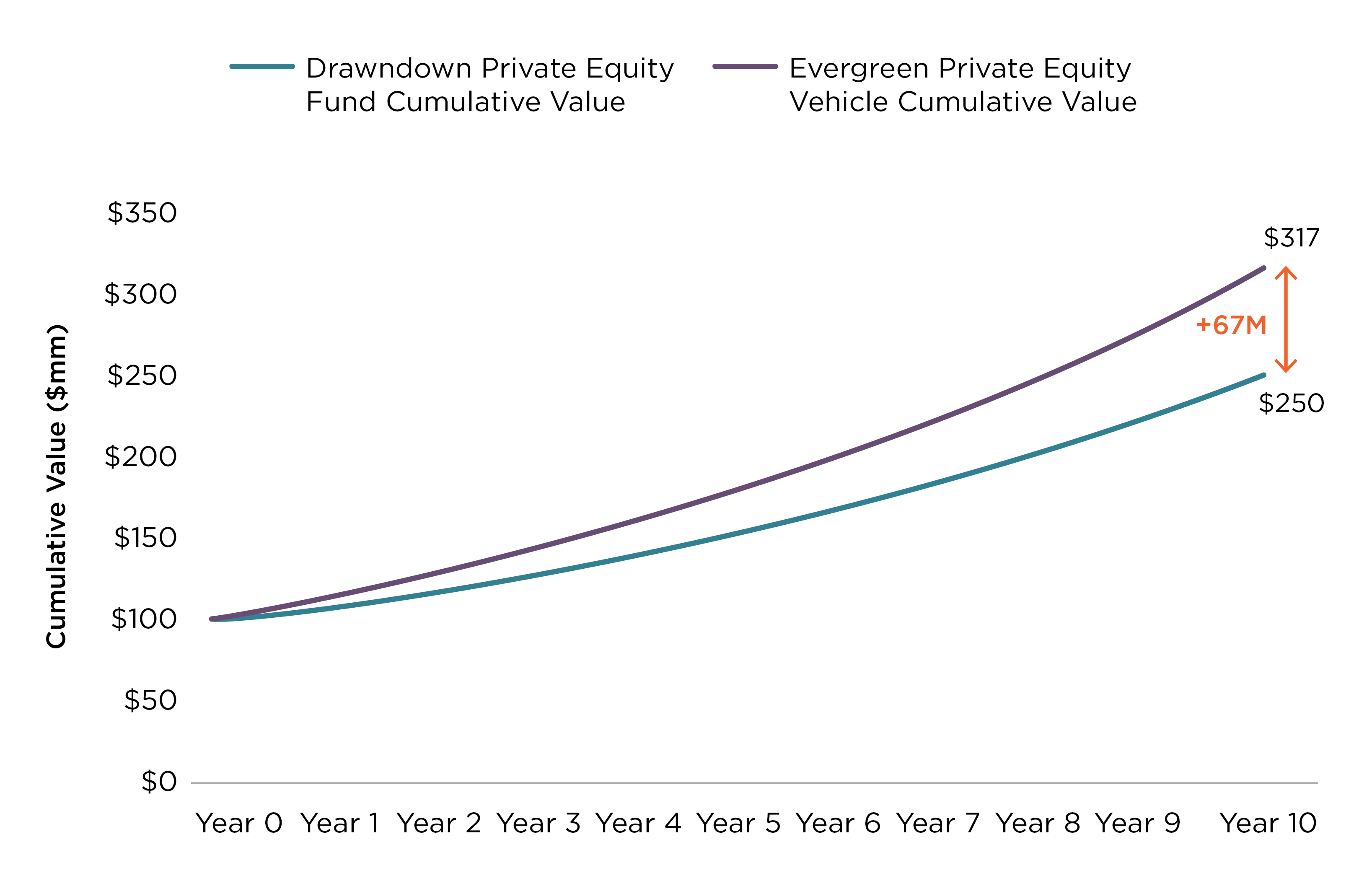

Research from KKR[3] shows that an evergreen PE strategy can match or even outperform the returns of traditional, drawdown-based PE strategies.

In addition to potentially higher returns, the evergreen model provides individual investors with two key advantages: initial access and ongoing liquidity, which are features not offered by traditional models.

Conclusion

This article has provided a brief overview of the advantages of evergreen funds. While they are not a “one-size-fits-all” solution, they offer something genuinely new and beneficial by expanding access to PE for both investors and companies looking to raise capital.

Data from Preqin reveals that the number of global evergreen funds grew significantly, doubling to over 500 between 2018 and 2023, with more than $350 billion in capital.[4] The fact that even institutional investors are considering evergreen funds underscores their legitimacy as a viable access point and as an effective approach to gaining exposure to private markets.

As the landscape evolves, we believe evergreen funds are an area worth monitoring closely in the future.

[2] Kohlberg Kravis Roberts & Co.